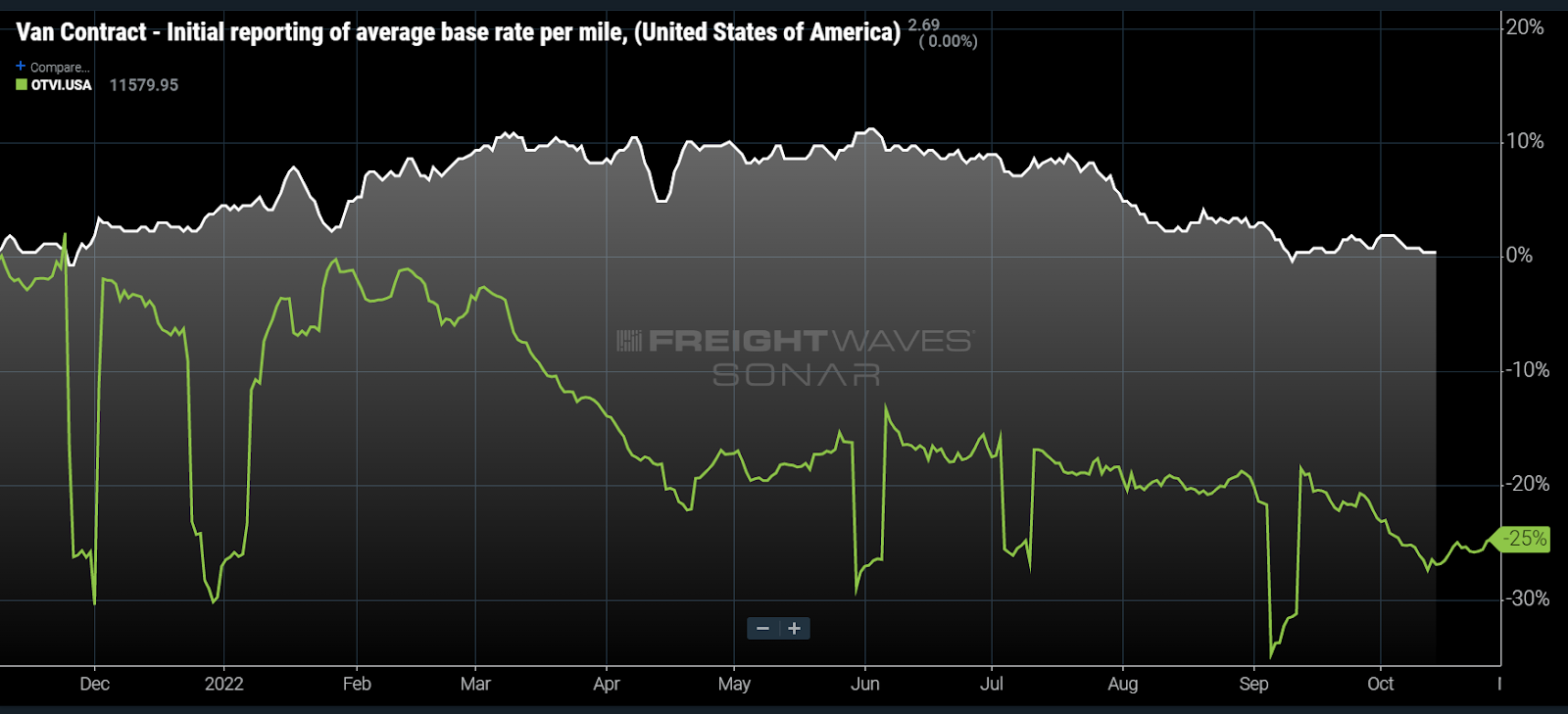

Chart of the Week: Van Contract Rate Initial Report, Outbound Tender Volume Index – USA SONAR: VCRPM1.USA, OTVI.USA

Dry van truckload contract rates have fallen about 9% since the start of the summer but have slowed their rate of descent this fall, according to FreightWaves’ Van Contract Initial Report Index (VCRPM1), which is based on the linehaul-only portion of freight invoices.

Is this a sign that shippers will not be aggressively peeling back the past two years of rate increases?

Dry van contract rates are still more than 35% higher than they were in June of 2020 but are essentially flat from a year-over-year (y/y) perspective. Contract rates “peaked” in June but were essentially flat from early March into July.

The pandemic-era tightness that began mid-2020 started an increasing trend of shorter cycle bids (aka mini-bids), which allowed contract rates to move faster than they historically have. Before 2020, the average bid cycle for shippers was around 12 months, meaning contract rates did not have strong fluctuations throughout the year.

The big question is how motivated or cognizant will shippers be as a sharp drop in demand has made capacity more easily attainable. The Outbound Tender Volume Index (OTVI) measures the total tenders or requests from shippers to carriers for capacity. Those requests are down 25% y/y.

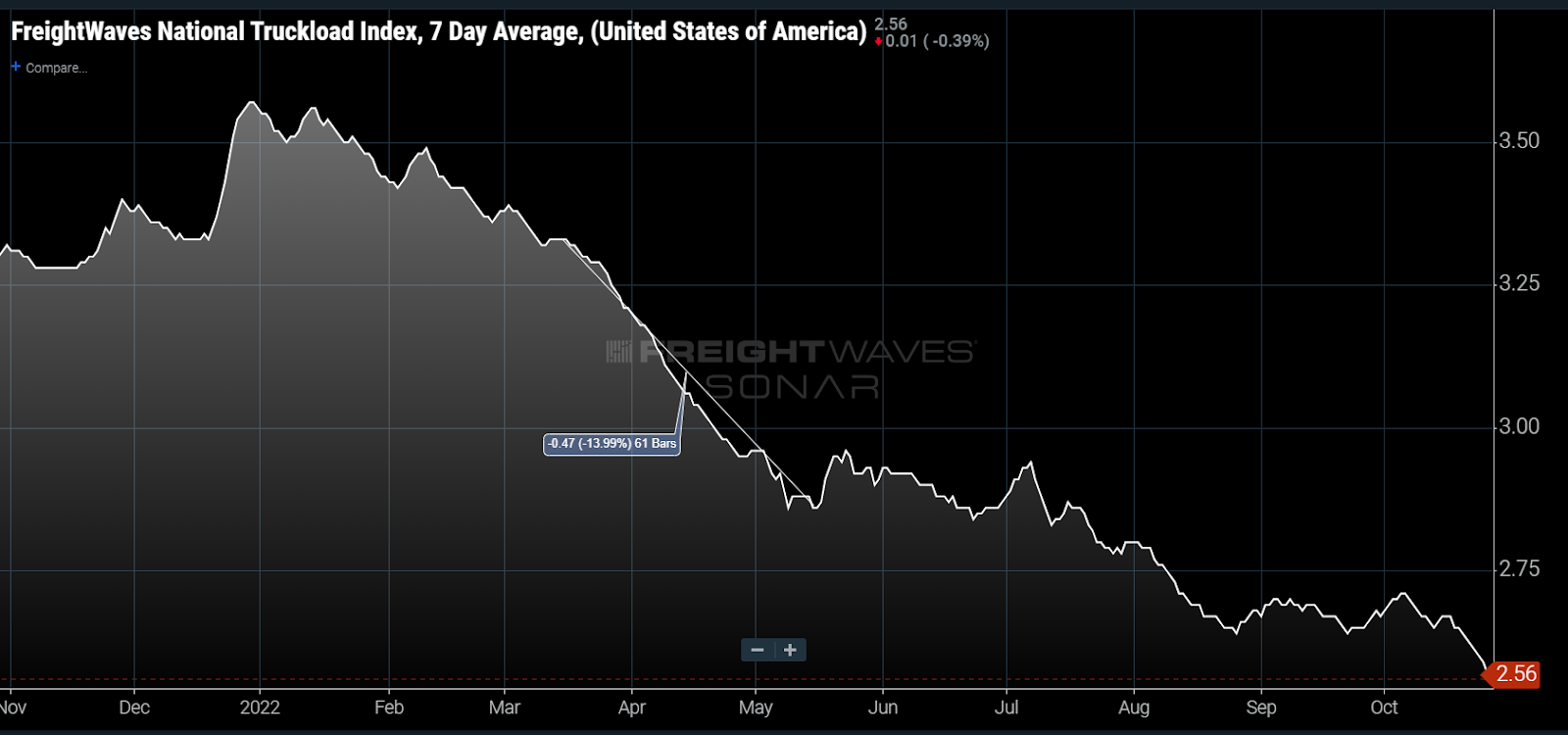

The truckload spot market responded quickly in March, with the National Truckload Index (NTI)…

{kind=link}