Key points:

- The US herd continues to decline, reducing a further 0.6% on the year to sit at 86.7 million head as of January 2025.

- Reduced supply continues to support domestic beef prices across the United States. In the week ending 7 February 2025, the five-area deadweight steer average was $7.19 /kg, up 87 cents (14%) on the year.

- Australia became the biggest supplier of United States beef imports in 2024.

- Tight US supplies coupled with strong demand on the global market are likely to lend support to UK prices, despite limited direct trading relationships between the UK and US.

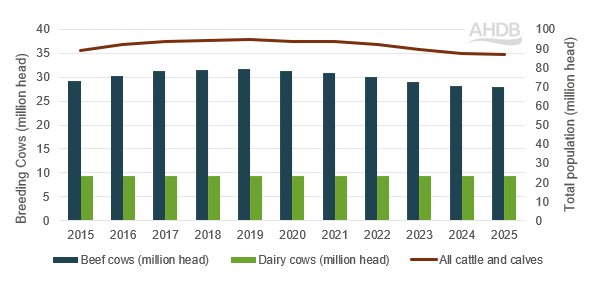

Supply

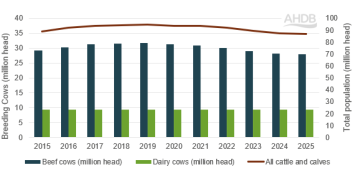

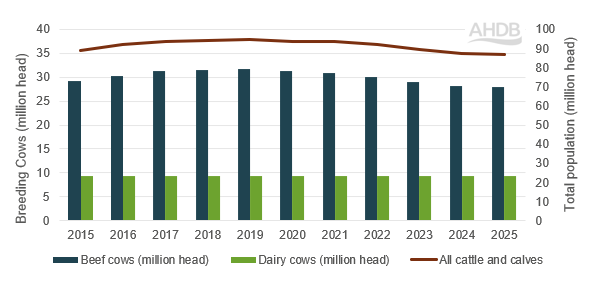

The beef herd in the United States has been in consistent decline since 2019, standing at 86.7 million head in the January 2025 inventory, down 0.6% on the year and down by 9% from 2019.

USA January cattle inventories

Source: USDA

The reasons for this long term contraction in supply are multiple; it is in part caused by the destocking phase of the cattle cycle, and also in part due to rising input costs and droughts forcing ‘cattle-calf’ operations to contract thus reducing the cattle available for feed-lots.

In their February 2025 outlook, the USDA reported that the ratio of beef heifer replacements to the previous year’s calf crop was continuing to fall as historically high beef prices encourage heifers onto the feeder market. This would suggest that the tightness in supply is likely to persist.

Production

In spite of this smaller herd going into 2025, US beef production…

{kind=link}